Why the Order of Returns Matters

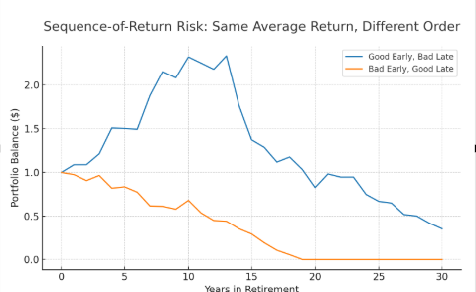

Imagine two retirees, Bob and Sam.

Both start with $1,000,000.

Both withdraw $40,000 per year.

Both earn an average return of 7% over 25 years.

On paper, their outcomes should be identical.

But they’re not. Bob retired before Sam did, under very different market conditions:

- Bob experienced strong markets early on, followed by downturns later in retirement

- Sam faced market losses early in retirement, with recovery happening years down the road

Despite receiving the same average return, Bob finishes with assets remaining…

while Sam risks running out of money years earlier.

In this scenario, Sam taking income during the downturn reduced his account balance, and the longevity of his retirement savings.

The difference isn’t discipline.

It isn’t strategy.

It’s timing.

This is known as sequence-of-returns risk—the risk that poor market performance early in retirement, combined with withdrawals, can have a lasting impact on a portfolio.

Why Sequence Risk Matters

Sequence risk is one of the most overlooked—and potentially consequential —risks in retirement:

- Same averages, very different outcomes

In fact, research consistently shows that retirees with identical portfolios and withdrawal rates can experience dramatically different results based solely on the order of returns. - It doesn’t show up in projections

Average return assumptions often mask this risk. Sequence presents itself only when income withdrawals begin—making it a challenge specific to those close to retirement and recently retired.

A Real World Example – The Lost Decade

The decade from 2000 through 2009 included multiple negative years—2000, 2001, 2002, and 2008—and produced approximately a –3% average annual return for the S&P 500 over the full 10 years. It’s often referred to as “The Lost Decade.”

For retirees drawing income during that period, the impact to their portfolio wasn’t temporary.

Withdrawals during market declines locked in losses and reduced the ability to rebound—even though markets eventually recovered.

What the Research Shows

The impact of sequence risk is well documented:

- Studies from Vanguard show that early down markets can significantly shorten the lifespan of a retirement portfolio, even when long-term average returns appear sufficient.

- Analysis from Morningstar highlights that retirees who adjust withdrawals during downturns can improve longevity of their portfolio.

- Other studies by GMO LLC have shown Sequence risk is a material driver of real-world investor outcomes, not captured in standard portfolio analysis

In short:

The timing of your retirementcan matter just as much as how you invest.

How to Reduce Sequence-of-Returns Risk

You can’t control what markets do—but you can control how your plan responds.

Here are three ways to better manage sequence risk:

1. Build income stability first

Cover your essential expenses with a ‘floor’ of reliable income—like Social Security, pensions, or annuity-based income—so you’re not forced to draw from investments during downturns.

2. Stay flexible with withdrawals

Instead of relying on a fixed rate like 4%, consider adjusting discretionary spending based on market conditions. Even small changes can make a meaningful difference over time.

3. Align your assets with purpose

Structure your portfolio with both stability and growth in mind. Having adequate liquid reserves can help you avoid selling investments at the wrong time.

Key Takeaways

- The 4% rule can be a helpful guideline—but it comes with risks and no guarantees

- Sequence-of-returns risk can impact savings longevity even when long-term averages look solid

- A plan built around stable income and flexibility can help improve long-term durability

A retirement strategy built on predictable baseline income helps reduce sequence risk by covering essential expenses first—so your portfolio is under less pressure and can stay focused on long-term growth.

Next Steps

If you’d like to better understand how sequence risk impacts your retirement:

- Start a conversation → (ADD Scheduling link)

- Reach out directly with questions → (ADD Phone, Email, Social links)

- Review our other articles → (LINK to blog page)

Research & Citations

- Vanguard Group

- Vanguard. “Fuel for the F.I.R.E.: Updating the 4% rule for early retirees.” (2021)

- Vanguard research consistently demonstrates that poor early returns materially increase portfolio failure rates, even when long-term averages are unchanged.

- Morningstar

- Blanchett, David. “Dynamic Spending in Retirement.” Morningstar Research (2015–2023 series)

- Findings show that flexible withdrawal strategies can significantly improve retirement sustainability, particularly during early downturns.

- GMO LLC

- Grantham, Jeremy & GMO Research Library

- Research highlights that valuation levels and return sequencing can have a greater impact on outcomes than static asset allocation assumptions.

- Financial Planning Association / Journal of Financial Planning

- Bengen, William (1994). “Determining Withdrawal Rates Using Historical Data.”

- Foundational research behind the 4% rule, demonstrating that sequence of returns is a primary driver of safe withdrawal outcomes.

- S&P 500 Index historical data

- 2000–2009 period commonly cited as the “lost decade,” with approximately –3% annualized returns, illustrating real-world sequence risk.

Compliance Footer

This material is for educational purposes only and is not intended as investment advice. All investing involves risk, including the potential loss of principal. Past performance is not indicative of future results. Strategies referenced may not be suitable for all individuals.

Last Updated 3/31/2026